To understand where prediction markets are in 2026, you have to understand where finance was in 1982.

The American equities market was emerging from a fifteen-year malaise. The Dow had spent the entire 1970s trapped between 600 and 1,000 points. Inflation was double-digit. Pension funds were dumping stocks for bonds. By August 1982, the bull market that would define the next two decades was just beginning, and almost no one realized it.

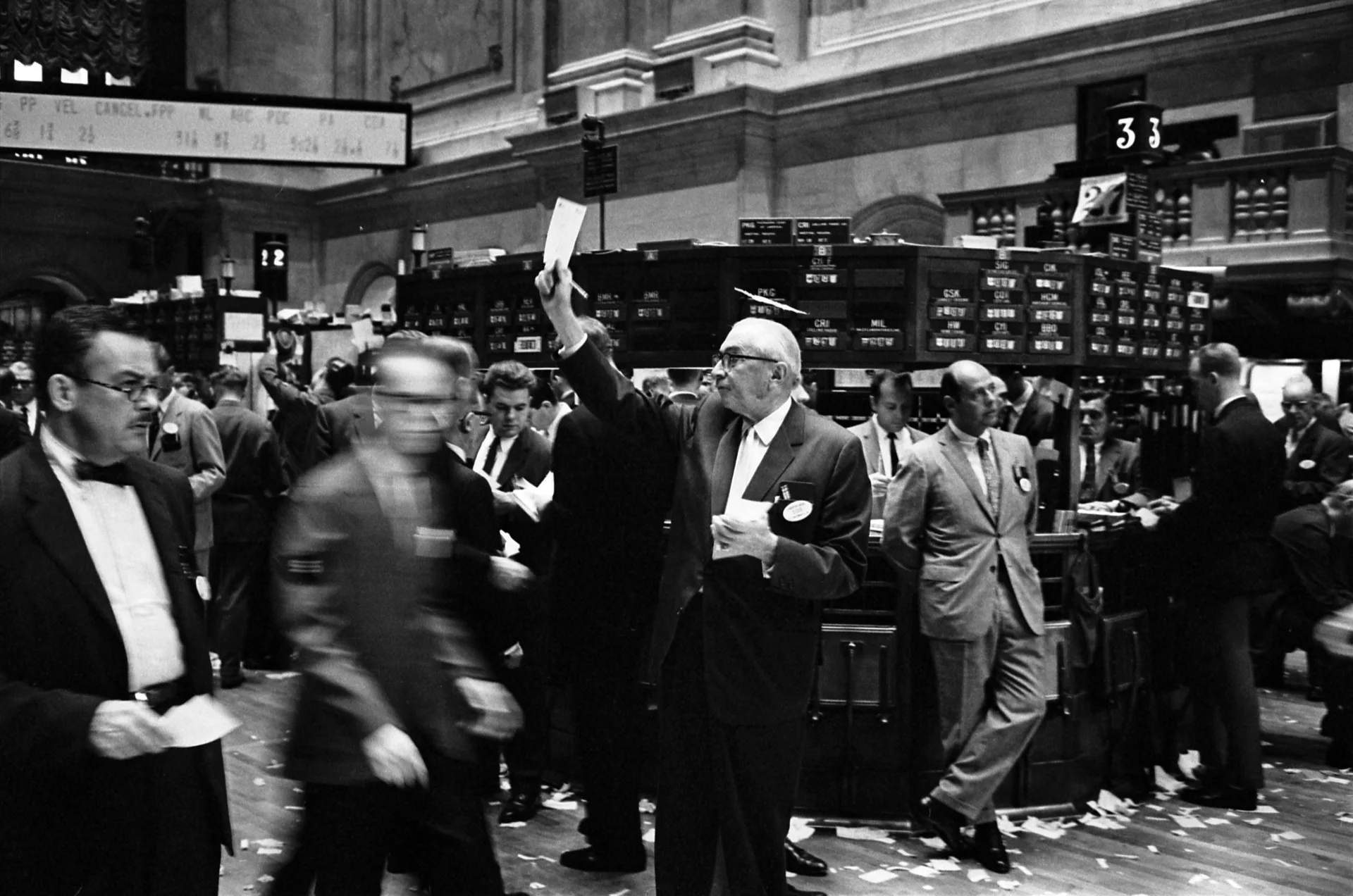

Underneath the surface, the market was bigger, faster, and more fragmented than its infrastructure could handle. The NYSE, the AMEX, NASDAQ's new electronic dealer network, and regional exchanges in Boston, Philadelphia, and the Pacific were each pricing the same securities at slightly different levels, at slightly different speeds, through slightly different protocols. There was no real-time, multi-venue view of anything. A trader who wanted to know the best bid on IBM had to call four desks.

Bond pricing was worse. Treasury yields were public, but corporate bond spreads, municipal pricing, and the entire over-the-counter universe lived inside the heads, and Rolodexes, of dealer salespeople. The buyer almost never saw the spread. Information asymmetry was the business model.

The trading floor itself was an analog system. Paper tickets. Runners. Telephones. A bond trader at Salomon Brothers in 1981 could not see what a bond trader at Goldman was bidding on the same CUSIP without making a call. The "wire," Reuters and Dow Jones, gave you headlines, but headlines are not prices.

And then, in December 1982, Michael Bloomberg delivered the first Market Master Terminal to Merrill Lynch.

The Terminal did not invent any new data. Every price it served already existed somewhere, on an exchange tape, in a dealer's notebook, in a regulatory filing. What it did was assemble that data into a single decision-support layer with a keyboard, a query syntax, and an answer in under a second.

That was the entire innovation. The market had outgrown its tools, and Bloomberg simply built the tool the market already needed.

By 1990, there were 10,000 Terminals on Wall Street. By 2000, 150,000. By 2026, 325,000 subscribers across 73 countries are processing 60 billion data points a day through Bloomberg's infrastructure. The Terminal did not just serve finance; it became the central nervous system of the entire industry. Traders, analysts, journalists, regulators, central bankers, every meaningful actor in global capital markets transacts on top of the same primitive.

That is what happens when a market outgrows its tools, and the right company shows up in the right year.